Does Making Minimum Payments Hurt Your Credit?

Making minimum payments on your credit card does provide benefits if you have emergency expenses or want to build your credit. But what is the long-term effect on your credit score if making minimum payments becomes a habit?

What Does it Mean to Make Minimum Payments?

Congratulations! You got approved for a credit card and are now free to make purchases up to a certain limit. Your card issuer will usually give you three options when it’s time to pay back what you spent for the month:

Make a minimum payment

Pay the statement balance

Pay the balance in full

Your minimum payment is normally a small percentage of your overall balance each month.

What Happens if You Only Pay the Minimum?

Making minimum payments on time helps you do three things:

Remain in good standing with your lender

Maintain a positive payment history with credit bureaus

Avoid late fees and derogatory marks on your credit report

At the end of the day, paying the minimum each month is a better option than making partial payments, or worse, making no payment at all.

Failing to make at least the minimum payment each month without an arrangement with your lender can and will be reported to credit bureaus as delinquent, meaning your credit score could take a significant hit.

How Making Minimum Payments Impacts Your Credit Score

You may already be familiar with the five most common factors affecting whether your credit score rises or drops a few points. Payment history, which we covered in the last section, is the most important.

The amount of credit you owe, or your credit utilization ratio, is the next most important factor and can cause your credit score to drop if mismanaged. This ratio looks back at what percentage of your revolving credit limits you are using. Any time your utilization rate goes above 30%, your credit score could be negatively impacted until you pay down your balances.

What does this mean if you’re someone used to making minimum payments?

UNDERSTANDING AND AVOIDING THE MINIMUM PAYMENT TRAP

Let’s be clear: paying the FULL balance each month on your credit card is the best option in the long run. But there may be months where you need the extra money to fix your car or pay a medical bill. In those cases, paying the minimum will cause you to carry a credit card balance that racks up interest charges on your purchases.

You can estimate your monthly interest charges using the following formula:

Divide your credit card’s annual percentage rate (APR*) by 12 (the number of months in a year) and multiply by your average balance.

For example: If your credit card’s interest rate is 23.99% APR*, the monthly interest rate would be 1.99% or 23.99 divided by 12. Carrying over a $3,000 balance means you would owe $59.70 worth of interest the next month on top of any additional purchases you make with the card.

If this happens, paying down your balance WILL take longer. You could end up paying more than your credit limit. Continuing to make purchases will also affect your credit utilization ratio if you only make minimum payments.

The interest will cause your balance to grow more than it decreases, and your credit score could drop.

If your interest rate gets as high as 23.99%, switch to Carolina Foothill FCU’s VISA Credit Card. We offer an introductory rate of 2.99% APR* for the first 12 months.

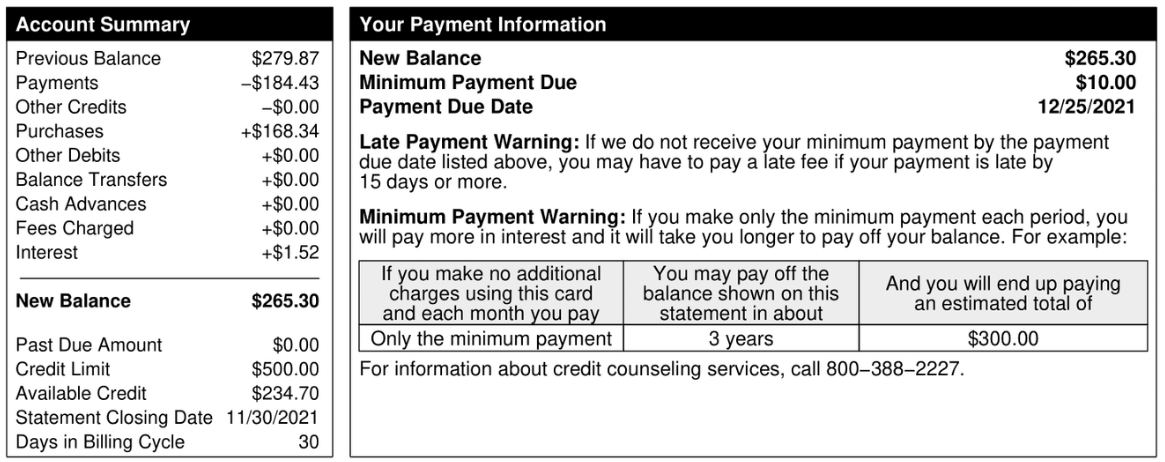

MINIMUM PAYMENTS WARNING

For those of you carrying a balance on your credit card, the Credit CARD Act made it a legal requirement for card issuers to include a “minimum payment warning” on their billing statements each month.

The “warning” includes a table explaining how long it will take you to pay your balance off if you only make minimum payments. Take a look at the image below.

How to Deal With Your Debt

The bottom line is this: dealing with your debt NOW will always be better than putting it off until later. Making minimum payments doesn’t have to be a financial habit you continue. We have a few tips that may encourage you to pay more each month.

DOUBLE YOUR CREDIT CARD PAYMENTS

Consider making double whatever your minimum payment is each month. The time it takes for you to pay off the remaining balance could be cut in half.

CREATE A BUDGET FOR YOUR MONEY AND STICK TO IT

Another option is accounting for every dollar you earn each month. Track your spending down to zero, create a budget, then contribute any extra cash to your monthly balance. You may not be making double payments, but paying more than the minimum will also accelerate your payoff date.

FIGURE OUT HOW TO CREATE MORE INCOME FOR YOURSELF

Remember, making minimum payments is better than collecting late fees that will damage your credit score and keep you in a financial pitfall.

Consider working a part-time job or developing a new side hustle to bring in extra money to pay down your debt even faster.

ASK FOR FINANCIAL ASSISTANCE

If you cannot afford to pay the minimum, here are five options that may help you:

Ask for a lower interest rate on your credit card or loan

Move your payment due date to better fit your payday

Move your debt to a new credit card with a low introductory interest rate on your first balance transfer for the first 12 months

Monitor your credit report to see where you stand (Experian, Credit Karma, AnnualCreditReport.com, etc.)

Visit the Carolina Foothills FCU E-Learning Library

Think of your long-term financial health when making monthly payments — hopefully more than the minimum.

You may also enjoy…